When it comes to Apple (AAPL), there are those who just don't like the company (or the stock). No matter what Apple does, the bears will criticize the company. Just last week, Apple had a great quarter and issued stronger than usual guidance. But guess what? It didn't seem good enough, and the Apple bears were out in full force. Even when Apple does something these people want, they find a way to criticize the company for it. Today, I'll take another look at Apple, and explain why the Apple bear crowd is getting really desperate.

The quarter was NOT disappointing:

Literally, just a few hours after Apple reported, and after my article above was published, this is what was seen on Yahoo! Finance's homepage. Look at the headline.

(click to enlarge)

(Source: Yahoo! Finance homepage)

This was the actual Reuters article that goes with that headline image. Here are the first two "paragraphs" from the article:

(Reuters) - Apple Inc's profit and margins slid despite selling 33.8 million iPhones in its September quarter, prompting a brief but sharp selloff as disappointed investors cashed in some of the stock's recent strong gains.

Wall Street had hoped for a stronger beat on quarterly sales after the company predicted in September that its revenue and margins would come in at the high end of its own forecasts.

The second part of that is absolutely hilarious. Apple originally guided to revenues of $34 billion to $37 billion, and gross margins of 36% to 37%. After the great iPhone weekend, Apple, as the article states, said that revenues and gross margins would be at the higher end of its ranges. What did Apple come in at? How about $37.47 billion and 37.02%, respectively. Apple came in half a billion above in terms of revenues and above the high end of the gross margin range. Apple beat analyst estimates for the iPhone, iPad, and Mac, its three most important lines. The only product category that missed was the iPod, whose unit sales totaled just 1.53% of Apple's quarterly revenues.

So how was this a disappointment? It wasn't. Apple beat by $630 million on the revenue front and $0.33 in earnings per share. Where does the Reuters article state this? The second and third to last sentences of the article. Yes, buried at the bottom, the fact that Apple crushed estimates. Sorry Apple bears, but trying to say this quarter was a disappointment is just wrong. Find someone else to pick on. Apple came in well above the high end of its revenue range, and above its gross margin guidance too. Oh, and unlike Microsoft (MSFT) or Google (GOOG), the beat wasn't fueled by dramatically lowered expectations. By the way, Google's beat was not as impressive, and yet the stock soared to new all-time highs. Google is certainly held to a different standard, and that is partially due to all of those Apple bears out there. Microsoft saw its revenue estimates come down by more than a billion between quarters and more than a dime for earnings. That didn't happen to Apple.

Guidance was very good:

Another complaint of Apple bears was that guidance, particularly gross margin guidance, was not very good. Well, Apple guided to a revenue midpoint of $56.5 billion, and the analyst estimate was $55.65 billion, so Apple was almost a billion ahead. Remember, for fiscal Q4 the original midpoint was $35.5 billion, and Apple beat that by nearly $2 billion. While Apple has been giving more realistic guidance in the past few quarters, the company still has been conservative to some extent.

So on to gross margins. The company guided to a midpoint of 37%, basically flat with Q4. This was seen as a huge negative, with many expecting a midpoint closer to 38%. Well, Apple detailed on the conference call an issue with deferred revenues. It was stated that about $900 million would be pushed into fiscal Q1, and that would hurt gross margins. Management stated that gross margin guidance would have been around 38.5% if not for the deferral. More on this in the next section. But even with the "light" guidance, I still calculated Apple's earnings per share, based on all guidance midpoints, at $13.51. That was below the $13.86 estimate, but I also did not assume any benefit from the buyback plan. Don't forget, Apple exceeded its fiscal Q4 guidance by anywhere from 60 to 90 cents in EPS, depending on what share count you used.

Also, if guidance was so disappointing, why have analysts raised their expectations since the report? Going into the report, as mentioned above, expectations were for $55.65 billion and $13.86, respectively. Current estimates call for $57.04 billion and $13.93, respectively. If Apple's guidance was disappointing, analysts would but cutting estimates, not raising them. As you can see from the table below, estimates were already rising into the report, so it's not like estimates were low to begin with.

Additionally, those that are criticizing Apple for weak margin guidance are the same that were arguing for a cheaper iPhone. Those are the people that didn't like the iPhone 5C, because it was priced too high. Well, if Apple had a cheaper phone, margins would have been lower. So the bears criticized Apple for not having a cheaper phone, and then also criticized Apple for low margins. You can't have it both ways.

Back to that deferred hardware revenue:

I want to get back to that $900 million in deferred revenue. Apple bears are pointing out that if it were not for that money, fiscal Q1 revenue guidance would be a bit lower, and perhaps the midpoint would only be in-line with analyst expectations. Well, if that were the case, and these revenues instead were booked in fiscal Q4, Apple would have produced a tremendous revenue beat, roughly $1.5 billion. Had Apple come in around $38.4 billion in revenues with in-line guidance, the bears would have criticized the guidance. But in that case, Apple would have had a tremendous Q4 beat. Again, you can't have it both ways. It was not a disappointing quarter, and guidance was not bad.

Domestic cash and stock buybacks:

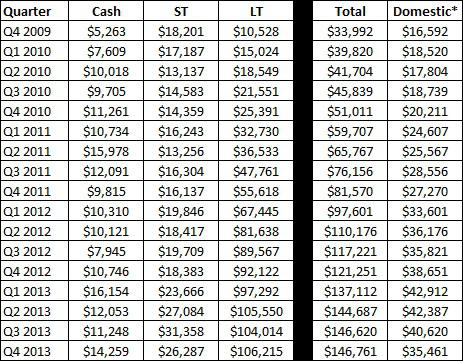

Apple's cash pile has been another hot spot for bears to attack the technology giant. There are those out there calling for Apple to better use its cash, primarily for capital returns. Carl Icahn is arguing for a $150 billion buyback. To this point, a larger buyback may be possible, but it all depends on the time frame (2 years, 5 years, 10 or more?). For this argument, I'm not calling Icahn an Apple bear, because he's been bullish on the stock, and also is invested in Apple. Well, the following table shows some key Apple cash pile statistics, with dollar values in millions.

*Number may be slightly off due to rounding of foreign balance.

Apple's domestic cash pile value declined by about $5 billion as Apple roughly bought back that much stock in fiscal Q4. The domestic cash pile is key, because it is the only fund Apple can use for dividends and buybacks. If Apple wants to use its foreign funds, more than $111 billion at the end of fiscal Q4, it has two choices. It can bring those funds back into the US, and face billions in repatriation taxes, or Apple can borrow against those balances. Apple issued $17 billion worth of debt earlier this year, to accelerate part of its buyback.

So what's up with Apple bears here? Well, a number of those people arguing for a larger buyback are those that are also criticizing Apple's earnings (especially in the last quarter or two) for being propped up by the buyback. Obviously, as Apple reduces its share count, earnings per share figures are helped. But again, you can't have it both ways. How can you argue that Apple needs a bigger buyback, then criticize it when earnings per share are helped by said buyback? Additionally, if Apple does take out debt and raises the buyback, don't criticize the company for having a weaker balance sheet.

Apple is expected to return about $100 billion to shareholders over a three year period between the dividend and the buyback. That is a tremendous amount, and should not be taken lightly. Apple has a little more than $37 billion left on the buyback ($22.86 billion worth of shares bought back already), and the company expects the buyback to be done by the end of calendar 2015. That means a little more than $4 billion can be spent on average over the next 9 quarters. Apple should generate enough cash over the next two years where it could pay the dividend (and raise it by a fair amount) and finish off the buyback without completely depleting its domestic cash balance. However, it would not surprise me if the company did issue a little more debt, just so it has the so-called "margin of safety" in its domestic cash pile.

In terms of increasing the buyback, I've already said Apple could easily do it, but play around with the timing. I'm on the record saying that Apple could raise the buyback to a trillion dollars, just with no expiration date. On average, Apple is going to buy back about $20 billion worth of stock a year for three years. That is a tremendous amount, and I wouldn't be arguing for them to increase the buyback into 2015. But once this current $60 billion plan is over, I expect the buyback to continue, so the current number could be "raised" with an extension of the timeline.

Top tier tech comparisons:

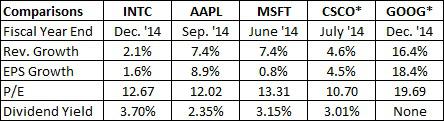

In many of my technology articles lately, I've shown comparisons between a number of the top tier tech names. These names include the three I've mentioned already here today, plus Intel (INTC) and Cisco Systems (CSCO). The following table shows a comparison of growth, valuation, and dividend yields.

*EPS and P/E numbers are non-GAAP.

What's the key takeaway here? Well, Apple might be the cheapest of any of these names, depending on what kind of conversion you use for Cisco's non-GAAP to GAAP earnings. But even if Apple and Cisco have the same valuation, Apple would be the better value thanks to its stronger growth profile and much larger buyback. Cisco is the only one of these names that has not reported earnings yet, as it has a slightly different fiscal year. Cisco will report on November 13th. When it comes to Intel, Apple seems like a much better investment. More growth at a cheaper price. Intel has risen a couple of percent since reporting its quarter, something Apple has not done. Intel issued worse than expected guidance, yet the stock still rose.

When it comes to Apple versus Google, Google provides more growth, but no dividend or buyback. Google also trades at nearly double the valuation when you convert Google earnings to GAAP. Google's stock has soared more than 15.5% since reporting earnings, despite a very small beat, and thanks to reduced expectations and a tax break. I mentioned above my article about Google being held to a different standard, and the company certainly is. Over the last two years, Google has missed revenue or earnings numbers several times, yet the stock is at all-time highs.

When it comes to Apple versus Microsoft, the two have comparable revenue growth, but Apple has more earnings growth. Microsoft has a higher dividend yield, but Apple has the more powerful buyback. Microsoft, however, trades at more than a 10% premium to Apple, thanks to Microsoft also rising after its earnings report. Microsoft's revenue and earnings beat was due to estimates being cut dramatically, although the company did issue decent guidance.

Despite decent growth and a very reasonable valuation, Apple is down almost 2% since its earnings report. The three other names that have reported have all risen since earnings. Personally, I think that is ridiculous, as Apple's beat was the most impressive.

Updating my Apple target:

I've gotten a ton of questions about my own price target for Apple since the earnings report, and I promised I'd be back in a week or so with an update. In my preview article for Apple's fiscal 2014, I set a target of $567 for the technology giant. As I have done in the past, I am providing a table of estimates and apply a multiple to each level of earnings. If you want to know what my price target is on any given day, look at the last table I provided, take the average earnings estimate from analysts, and do the math. Here's the table.

One quick note on these numbers. At current, I am not assuming an Apple-China Mobile (CHL) deal for my valuation. Obviously, a deal with China Mobile would be extremely positive for Apple. I think a deal is worth about 10%, so if a deal were to happen, you could basically up my target by 10%. As of Sunday, the average analyst estimate for earnings was $43.27. That gives me a price target of about $587, a $20 increase from my last update. Why have I upped my target? Well, here are the reasons why:

- Q4 report was strong and guidance was solid.

- iPad sales came in strong despite no refresh this spring.

- Company is buying back stock a little faster than I expected.

As of Sunday, I was basically in between the mean and median price target among Wall Street analysts. My target still implies about 13% of upside from here. You'll also notice that I am not one calling for Apple to be a $1,000 stock, or for it to be a $200 stock. I'm giving a fair representation of where I think Apple will go by the time it reports fiscal Q4 next year. For those that ask, my target including a China Mobile deal is about $645 right now.

Final thoughts:

It seems that the Apple bears are getting really desperate. Apple's Q4 earnings report was not disappointing, as the company raised its guidance during the quarter then beat it nicely anyway. Apple's guidance for fiscal Q1 was very strong as well. The Apple bears are doing whatever they can to discredit this name. They will argue that Apple needs a cheaper phone, but then they complain over margins. The bears complain that Apple needs a larger buyback, but then criticize Apple's earnings for being boosted by said buyback. Apple is the most profitable large cap US tech name, yet it is treated the worst. Apple bears are getting really desperate after another solid quarter, and I believe Apple's stock does go higher from here.

Additional disclosure: Investors are always reminded that before making any investment, you should do your own proper due diligence on any name directly or indirectly mentioned in this article. Investors should also consider seeking advice from a broker or financial adviser before making any investment decisions. Any material in this article should be considered general information, and not relied on as a formal investment recommendation.

via apple - Google News http://news.google.com/news/url?sa=t&fd=R&usg=AFQjCNETf-yZWtjxx69Q5y1HbuMSTs2IEw&url=http://seekingalpha.com/article/1800832-apple-bears-getting-really-desperate?source%3Dgoogle_news

0 comments:

Post a Comment